S-1: General form of registration statement for all companies including face-amount certificate companies

Published on August 29, 2014

As filed with the Securities and Exchange Commission on August 29, 2014

Registration Statement No. 333-__________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER

SYSOREX GLOBAL HOLDINGS CORP.

(Exact name of Registrant as specified in its charter)

|

Nevada

|

7379

|

88-0434915

|

||

|

(State or other jurisdiction of

incorporation or organization)

|

(Primary Standard Industrial

Classification Code Number)

|

(I.R.S. Employer

Identification No.)

|

3375 Scott Blvd., Suite 440

Santa Clara, CA 95054

Telephone: 408-702-2167

Telecopier: 408-824-1543

(Address and telephone number of principal executive offices)

Mr. Nadir Ali, CEO

3375 Scott Blvd., Suite 440

Santa Clara, CA 95054

Telephone: 408-702-2167

Telecopier: 408-824-1543

(Name, address and telephone number of agent for service)

Copy to:

|

Kevin Friedmann, Esq.

|

|

Richardson & Patel LLP

|

|

1100 Glendon Avenue, Suite 850

|

|

Los Angeles, CA 90024

|

|

Telephone: (310) 208-1182

|

Approximate Date of Proposed Sale to the Public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. þ

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer

|

o

|

Accelerated filer

|

o

|

|

Non-accelerated filer

|

o

|

Smaller reporting company

|

þ

|

|

(Do not check if a smaller reporting company)

|

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of

Securities to be Registered

|

Amount to be

Registered (1)

|

Proposed

Maximum

Offering Price

Per Share (2)

|

Proposed

Maximum

Aggregate

Offering Price

|

Amount of

Registration Fee

|

||||||||||||

|

Shares of Common Stock, par value $0.001 per share

|

5,628,886

|

$

|

3.68

|

$

|

20,714,300

|

$

|

2,668

|

|||||||||

|

Shares of Common Stock, par value $0.001 per share, underlying warrants

|

139,584

|

$

|

3.68

|

$

|

513,669

|

$

|

66

|

|||||||||

|

5,768,470

|

$

|

21,227,969

|

$

|

2,734

|

||||||||||||

|

(1)

|

Pursuant to Rule 416 under the Securities Act of 1933, as amended, the shares being registered hereunder include such indeterminate number of shares of common stock, as may be issuable with respect to the shares being registered hereunder as a result of stock splits, stock dividends or similar transactions.

|

|

(2)

|

Estimated solely for purposes of calculating the registration fee pursuant to Rule 457(c) under the Securities Act of 1933, as amended, using the average of the high and low prices for the registrant’s common stock reported on the Nasdaq Capital Market on August 27, 2014.

|

This Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED AUGUST 29, 2014

Prospectus

5,768,470 Shares of Common Stock

Sysorex Global Holdings Corp.

This prospectus relates to the offer and sale of up to 5,768,470 shares of common stock, par value $0.001, of Sysorex Global Holdings Corp., a Nevada corporation (the “Company,” “Sysorex,” “us,” “our,” or “we”) by the selling stockholders identified on page 40 of this prospectus (the “Offering”).

We are not selling any securities under this prospectus and will not receive any of the proceeds from the sale of shares by the selling stockholders.

The selling stockholders may sell the shares of common stock described in this prospectus in a number of different ways and at varying prices. See “Plan of Distribution” for more information about how the selling stockholders may sell the shares of common stock being registered pursuant to this prospectus.

We will pay the expenses incurred in registering the shares, including legal and accounting fees. See “Plan of Distribution”.

We are an “emerging growth company” under the Federal Securities laws and are subject to reduced public company reporting requirements as set forth on page 5 of this prospectus. Our common stock is currently quoted on the Nasdaq Capital Market under the symbol “SYRX”. On August 27, 2014, the last reported sale price of our common stock on the Nasdaq Capital Market was $3.65. All historical share and per share data in this prospectus give effect to a reverse stock split effected on April 8, 2014.

Our business and an investment in our securities is speculative and involves a high degree of risk. See “Risk Factors” beginning on page 9 of this prospectus for a discussion of information that you should consider before investing in our securities.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR PASSED UPON THE ACCURACY OR ADEQUACY OF THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The date of this prospectus is , 2014.

ADDITIONAL INFORMATION

You should rely only on the information contained or incorporated by reference in this prospectus and in any accompanying prospectus supplement. No one has been authorized to provide you with different information. The shares are not being offered in any jurisdiction where the offer is not permitted. You should not assume that the information in this prospectus or any prospectus supplement is accurate as of any date other than the date on the front of such documents.

|

Page No.

|

|

|

1

|

|

|

8

|

|

|

9

|

|

|

39

|

|

|

40

|

|

|

44

|

|

|

45

|

|

|

46

|

|

|

73

|

|

|

89

|

|

|

95

|

|

|

98

|

|

|

100

|

|

|

102

|

|

|

105

|

|

|

106

|

|

|

106

|

|

|

F-1

|

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement that we filed with the Securities and Exchange Commission (the “SEC”) using the SEC’s registration rules for a delayed or continuous offering and sale of securities. Under the registration rules, using this prospectus and, if required, one or more prospectus supplements, the selling stockholders named herein may distribute the shares of common stock covered by this prospectus. A prospectus supplement may add, update or change information contained in this prospectus.

The following summary highlights information contained elsewhere in this prospectus. This summary may not contain all of the information that may be important to you. You should read this entire prospectus carefully, including the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our historical financial statements and related notes included elsewhere in this prospectus. In this prospectus, unless otherwise noted, the terms “Sysorex”, “the Company,” “we,” “us,” and “our” refer to Sysorex Global Holdings Corp., and its subsidiaries, Sysorex Federal, Inc., Sysorex Government Services Inc., Sysorex Arabia LLC, Lilien Systems, Shoom, Inc. and AirPatrol Corporation.

Except where otherwise indicated, all share and per share data in this prospectus reflect a one-for-two reverse stock split effected on April 8, 2014.

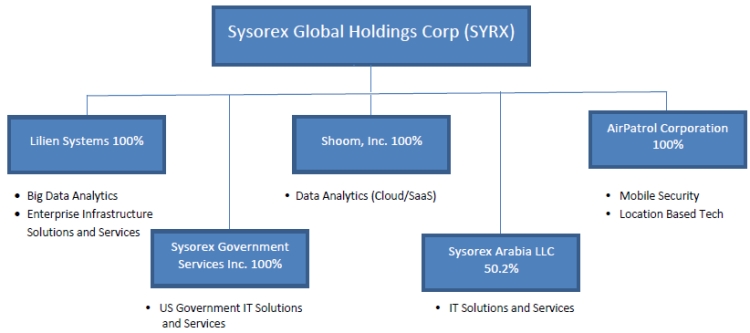

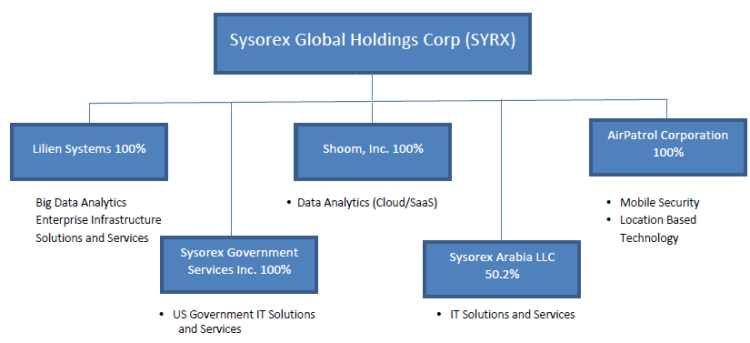

The Company

The following organizational chart sets forth the four subsidiaries of Sysorex Global Holdings Corp. and the lines of business in which they are engaged, as described below:

Overview

Sysorex Global Holdings Corp. provides a variety of IT services and technologies that enable customers to manage, protect and monetize their enterprise assets whether on-premise, in the Cloud, or via mobile. Historically our revenues were earned from customer bases 100% in the public sector but that has changed significantly with the acquisitions we have made since 2013. Currently, approximately 90% of the revenues we earn are from commercial enterprises and only approximately 10% are from government agencies. Our goal is to continue to build our private and public sector offerings and contracts. We intend to do this by acquiring other businesses.

On March 1, 2013, we acquired Lilien Systems, an enterprise IT infrastructure solutions provider with over $40 million in annual revenue, in consideration of a combination of $6,000,000 in value of common stock and $3 million in cash from debt financing (the “Lilien Acquisition”).

On August 31, 2013, we acquired Shoom, Inc. (“Shoom”) a provider of Cloud-based data analytics and enterprise solutions to the media, publishing, and entertainment industries with over $4 million in annual revenue with a retention rate of approximately 90% (over the last five years) in consideration of a combination of 1,381,000 shares of common stock and $2.5 million in cash (the “Shoom Acquisition”). The cash portion was funded by the excess working capital we obtained from the Shoom Acquisition.

On April 18, 2014, we acquired AirPatrol Corporation (“AirPatrol”), a developer of mobile device identification and locating systems pursuant to an Agreement and Plan of Merger, dated December 20, 2013, as amended for consideration equal to (a) $10,000,000 in cash, subject to certain adjustments, allocated to and among certain creditors, payees and holders of AirPatrol’s issued and outstanding capital stock and (b) 2,000,000 shares of Company common stock, subject to certain adjustments (the “AirPatrol Acquisition”).

The acquisitions of Lilien, Shoom and AirPatrol have expanded our depth of enterprise service offerings, including Big Data services and Cloud-based advanced analytics, while providing premier partnership status with leading vendors in IT infrastructure. Shoom also provides Sysorex with secure Cloud-based software products, which result in higher gross margins. These acquisitions reflect our business strategy, the purpose of which is to transform Sysorex from a services company to a technology company. We believe the acquisition of Lilien provides us with an opportunity for vertical market and geographic expansion. We are focusing our primary efforts on the U.S. market in the near-term. We have a small operating unit in Saudi Arabia and we may seek new contracts there. This unit does not represent a significant portion of our business and a failure to obtain contracts from our Saudi Arabian unit will not have a material impact on our revenues or operations.

Cyber security and Big Data analytics are the areas we are targeting because we believe, based on industry data that these are growing market segments. For example, security of all forms, especially cyber-security, are significant growth areas (Source: Market Research Media - U.S. Federal Cyber-Security Market Forecast 2013-2018 dated April 12, 2013), and Sysorex intends to increase its role in this sector. Gartner, Inc., an information technology research and advisory company, predicts that by 2015, 20% of Global 1000 organizations will have established a strategic focus on information infrastructure equal to that of application management. This is one of five Gartner predictions about Big Data and information infrastructure discussed in “Predicts 2013: Big Data and Information Infrastructure;” a November 30, 2012 report that describes in detail how the Big Data phenomenon will affect organizations, resources and information infrastructure. Our plan is to acquire companies with unique technologies and possibly some with patents, which we believe will give us an advantage over our competitors. However, the IT services and technologies industry is extremely competitive and many of the providers in the industry are extremely large and well financed. Therefore, there is a risk that the technologies we acquire or develop could become obsolete if others in the industry develop better products.

Recent events in the federal government including the recent budget impasse and sequestration can impact our business with the federal government if they re-occur. However, our government contracts are less than 10% of our total revenues. Specifically, Congressional action could delay payment on our current contracts, delay the award of contracts that Sysorex has under submission and delay the release of task orders from the government on its contracts including the US Navy SPAWAR contract discussed below. We believe both of these will be growth areas for the government despite budget challenges because of the increased need for solutions in this space, which is reflected in recent high profile events, such as the NSA information leaks by Edward Snowden and the LexisNexis information leaks, including the social security number of the United States First Lady along with millions of other Americans, that have made it more of a focus. Our government contracts are typically three to five years and we believe that our recent historical government contract revenues will be indicative of future government contact based revenues. New contracts would be accretive.

Lilien’s revenues are typically driven by purchase orders that are captured every month. Approximately 25% of these purchase orders are contracts that range from one to five years for warranty and maintenance support and are recurring. For these contracts the customer is invoiced one time and pays Lilien upfront for the full term of the warranty and maintenance contract. The unearned revenue is recorded as deferred revenue and amortized over the contract period. Lilien has a 29-year history and track record with a management team that we expect will continue to successfully generate and grow Lilien’s business. Lilien also has a high repeat customer rate of approximately 60% annually. Lilien’s revenues are diversified over hundreds of customers and no one customer exceeds 15% of its revenues. We believe this diversification provides stability to Lilien’s revenue streams.

Shoom’s software-as-a-service (SaaS) contracts are typically performed for periods of one or more years and Shoom has a high customer retention rate. Shoom offers eSolutions including eTearsheets, invoicing, CRM, and other products and services to 750 newspapers in the Cloud. Cloud or SaaS based analytics is a growing market that Sysorex intends to pursue beyond the media vertical that Shoom is in today. According to industry sources, Cloud based business analytics and business intelligence is expected to grow from $5.2 billion in 2013 to $16.52 billion in 2018 a 25.8% CAGR (Source: PRWeb Article - Cloud Analytics Market is Growing at an Estimated CAGR of 25.8% & to Reach $16.52 Billion by 2018 - New Report by Markets and Markets April 2, 2013.) Shoom has been in business for over 10 years and has been providing its Cloud solutions for over four years.

The Lilien Acquisition significantly impacted our results of operations for the year ended December 31, 2013, as indicated under “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” The results show a net loss which was attributable, in part, to certain one-time non-recurring charges related to the Lilien Acquisition and Shoom Acquisition, resulting in the Company incurring significant legal, accounting, due diligence, financing and general and administrative expenses as compared to the expenses incurred in the comparable period in 2012.

We believe the accretive impact of our acquisition strategy is becoming evident and the year ended December 31, 2013 included ten months of Lilien’s revenues and four months of Shoom’s revenues. We anticipate synergies and operational efficiencies to improve revenues for both Sysorex and Lilien, especially in Q3 and Q4 when Lilien’s business is historically stronger as a result of customer budgeting processes. Sysorex’ U.S. government operations are profitable and this division is expected to grow based on the U.S. Navy SPAWAR contract awarded to Sysorex earlier this year. The U.S. Navy SPAWAR contract started releasing task orders in Q1 2014 and other awards are expected later in the year, now that the current budget impasse is resolved. With the addition of Shoom we believe that our liquidity will improve significantly as Shoom’s business model generates approximately 78% gross margins. We believe that our shift to technology based business lines like Shoom and other future acquisitions will increase our customer base and, in turn, increase revenues to a level that will allow us to achieve profitability.

Our recent acquisition of AirPatrol, a developer of location-based cybersecurity and commercial services systems for mobile devices, on April 18, 2014, has provided the Company with the opportunity to expand its capabilities into location-based detection products. AirPatrol is a developer of mobile device identification and locationing systems. Its flagship product, ZoneDefense, is a security platform for wireless and cellular networks that can detect, monitor and manage the behavior of smartphones, tablets, laptops and other mobile devices based on their location. AirPatrol also offers a business-to-consumer platform called ZoneAware that allows retailers, resort owners, consumer firms and others to deliver custom content and services based on a mobile device’s location. We believe AirPatrol will leverage the analytics capabilities of Lilien and Shoom to drive new location data offerings.

Corporate Strategy

Sysorex management has a mergers and acquisitions strategy to acquire companies and innovative technologies servicing the multi-billion dollar IT industry. We have targeted services and technology/IP based companies since we believe that they add significant value to the Company. Sysorex plans to facilitate and manage cross-selling opportunities among the companies and provide shared corporate services to create efficiencies and be cost effective. We are seeking opportunities with the following profiles:

|

|

·

|

Innovative and commercially proven technologies primarily in cyber-security, business intelligence/analytics, Big Data services, Cloud and mobile/bring your own device (BYOD).

|

|

|

·

|

Commercial and government IT service companies which have an established customer base and are seeking growth capital to expand their capabilities, product offerings and substantially increase their revenues and operating profits.

|

|

|

·

|

Companies with proven technologies that are complementary to the Company’s overall strategy. We are looking at companies primarily in the United States. However, we may expand in our existing markets (e.g., Middle East) and into other geographies such as India and Europe, if there are significant strategic and financial reasons to do so.

|

An important element of our mergers and acquisitions strategy is to acquire companies with complementary capabilities/technologies and an established customer base in each of the above categories. We believe that the customer base of each potential acquisition will present an opportunity to cross-sell solutions to the customer base of other acquired companies.

Another important criterion is an acquisition candidate’s contract backlog. This is one of the most important benefits of having public sector clients. These customers provide very large multi-year contracts that can provide secure revenue visibility typically for three to five years. Based on management’s experience, we understand government contracting very well and have built a core competency in bidding on government requests for proposals. We are actively seeking companies that have built a backlog with various government agencies that can complement Sysorex’s existing contracts.

We intend to acquire innovative technologies and established, reputable IT services companies, using restricted common stock, cash and debt financing in combinations appropriate for each potential acquisition.

Industry Overview

Worldwide, companies and organizations are expected to spend a combined $3.8 trillion on hardware, software, IT services and telecommunications in 2014 with approximately 3.1% growth rate over the next five years (Source: Gartner, Inc. January 6, 2014 press release).

The U.S. Government spends approximately $80 billion in IT annually and this level of spending is expected to continue at a 3% compound annual growth rate (CAGR), compared with 6% historically in the first decade of the 21st Century (Source: Market Research Media - U.S. Federal IT Market Forecast 2013-2018). Security of all forms, especially cyber-security, are significant growth areas, and Sysorex intends to increase its role in this sector (based on: Market Research Media - U.S. Federal Cyber-Security Market Forecast 2013-2018 dated April 12, 2013). The focus is on deployment of technologies that proved their worth in the private sector. The technology segments like business intelligence, Cloud computing, eDiscovery, GIS and geospatial, non-relational database management systems, smart grid, SOA, unified communications and virtualization are expected to have double digit growth in the period 2013 – 2018 (Source: Market Research Media - U.S. Federal IT Market Forecast 2013-2018). The total annual U.S. Federal IT market is expected to surpass $93 billion by 2018 (Source: Market Research Media - U.S. Federal IT Market Forecast 2013-2018).

Implications of Being an Emerging Growth Company

As a company with less than $1.0 billion in revenue during our most recently completed fiscal year, we qualify as an “emerging growth company” as defined in Section 2(a) of the Securities Act of 1933, as amended, which we refer to as the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As an emerging growth company, we may take advantage of specified reduced disclosure and other requirements that are otherwise applicable, in general, to public companies that are not emerging growth companies. These provisions include:

|

|

·

|

Reduced disclosure about our executive compensation arrangements;

|

|

|

·

|

No non-binding shareholder advisory votes on executive compensation or golden parachute arrangements;

|

|

|

·

|

Exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting; and

|

Reduced disclosure of financial information in this prospectus, limited to two years of audited financial information and two years of selected financial information.

As a smaller reporting company, each of the foregoing exemptions is currently available to us. We may take advantage of these exemptions for up to five years or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company if we have more than $1.0 billion in annual revenues as of the end of a fiscal year, if we are deemed to be a large accelerated filer under the rules of the Securities and Exchange Commission, or if we issue more than $1.0 billion of non-convertible debt over a three-year-period.

The JOBS Act permits an emerging growth company to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We are choosing to “opt out” of this provision. Therefore, we will be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies.

Corporate Information

We were incorporated in the State of Nevada in April 1999, under the name Liquidation Bid, Inc., and we subsequently changed our name to Sysorex Global Holdings Corp. pursuant to a July 2011 merger with Sysorex Federal, Inc. and its wholly-owned subsidiary Sysorex Government Services Inc. Our principal executive offices are located at 3375 Scott Blvd., Suite 448, Santa Clara, CA 95054, and our telephone number is (408) 702-1267. Our subsidiaries maintain offices in Herndon Virginia, Larkspur California, Encino California, Maple Lawn Maryland, and Riyadh, Saudi Arabia. Our Internet website is www.sysorex.com. The information on, or that can be accessed through, our website is not part of this prospectus, and you should not rely on any such information in making any investment decision relating to our common stock.

The Offering

|

Securities Offered

|

5,768,470 shares of Sysorex common stock offered by the selling stockholders, including 139,584 shares of common stock underlying warrants.

|

|

|

Common Stock Outstanding

|

19,630,339 shares as of August 27, 2014 (1)

|

|

|

Common Stock to be Outstanding Immediately after the Offering

|

19,630,339 shares (2)

|

|

|

Terms of the Offering

|

The selling stockholders will determine when and how they will sell the common stock offered in this prospectus. The selling stockholders will sell at prevailing market prices through the Nasdaq Capital Market, or at privately negotiated prices in transactions that are not in the public market.

|

|

|

Termination of the Offering

|

The offering will conclude upon the earliest of (i) such time as all of the common stock has been sold pursuant to the registration statement or (ii) such time as all of the common stock becomes eligible for resale without volume limitations pursuant to Rule 144 under the Securities Act, or any other rule of similar effect.

|

|

|

Trading Market

|

Our common stock is traded on the Nasdaq Capital Market under the symbol “SYRX”.

|

|

|

Use of Proceeds

|

We are not selling any shares of the common stock covered by this prospectus. As such, we will not receive any of the offering proceeds from the registration of the shares of common stock covered by this prospectus.

|

|

|

Dividend Policy

|

We have never declared any cash dividends on our common stock. We currently intend to retain all available funds and any future earnings for use in financing the growth of our business and do not anticipate paying any cash dividends for the foreseeable future. See “Dividend Policy.”

|

|

|

Risk Factors

|

The common stock offered hereby involves a high degree of risk, and investors should read and consider these risks before making an investment decision. See “Risk Factors” beginning on page 9.

|

|

|

Reverse Stock Split

|

We completed a one-for-two reverse stock split of our common stock on April 8, 2014. All share counts in this prospectus are shown on a post-reverse stock split basis.

|

|

(1)

|

Includes up to 7,516 shares of common stock reserved for issuance to all former shareholders of Shoom, Inc., some of whom have not yet exchanged certificates representing their shares.

|

|

(2)

|

Excludes shares issuable upon exercise of outstanding options and warrants, and issuances of additional shares of common stock subsequent to August 27, 2014.

|

Summary Financial Information

The summary financial information set forth below is derived from the more detailed audited consolidated financial statements of the Company appearing elsewhere in this prospectus. You should read the summary consolidated financial information below in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements, including their footnotes.

Statement of Operations Data:

|

Six Months

Ended

June 30,

2014 |

Years Ended December 31,

|

|||||||||||

|

(Unaudited)

|

(Audited)

|

|||||||||||

|

2013

|

2012

|

|||||||||||

|

Revenues Net

|

$ |

33,464,618

|

$ | 50,571,557 | $ | 4,237,789 | ||||||

|

Cost of Revenues

|

$ |

23,434,213

|

$ | 38,317,246 | $ | 2,344,592 | ||||||

|

Gross profit

|

$ |

10,030,405

|

$ | 12,254,311 | $ | 1,893,197 | ||||||

|

Total Operating Expenses

|

$ |

13,095,197

|

$ | 16,170,215 | $ | 2,348,611 | ||||||

|

Loss from Operations

|

$ |

(3,064,792

|

) | $ | (3,915,904 | ) | $ | (455,414 | ) | |||

|

Other Income (expense)

|

$ |

(186,580

|

) | $ | (619,558 | ) | $ | (329,211 | ) | |||

|

Provision for income taxes

|

$ | (35,000 | ) | $ | - | $ | - | |||||

|

Net (Loss) Income

|

$ |

(3,286,372

|

) | $ | (4,535,462 | ) | $ | (784,625 | ) | |||

|

Net (Loss) Income Attributable to Non-Controlling Interest

|

$ |

(98,173

|

) | $ | (272,058 | ) | $ | (90,779 | ) | |||

|

Dividends

|

$ | - | $ | - | $ | - | ||||||

|

Net Loss Attributable to Stockholders of Sysorex

|

$ |

(3,188,199

|

) | $ | (4,263,404 | ) | $ | (693,846 | ) | |||

|

Net Loss Per Share - Basic and Diluted

|

$ |

(0.19

|

) | $ | (0.17 | ) | $ | (0.04 | ) | |||

|

Weighted Average Number of Shares Outstanding

|

16,455,268

|

24,575,556 | 17,962,586 | |||||||||

|

Basic and diluted net loss per share

|

$ |

(0.19

|

) | $ | (0.35 | ) | $ | (0.08 | ) | |||

|

Weighted average number of basic and diluted common shares outstanding

|

16,455,268

|

12,287,778 | 8,981,293 | |||||||||

Balance Sheet Data:

|

June 30,

|

December 31,

|

|||||||||||

|

2014

|

2013

|

2012

|

||||||||||

|

(Unaudited)

|

(Audited)

|

|||||||||||

|

Cash and Cash Equivalents

|

$ | 4,932,846 | $ | 2,103,955 | $ | 8,301 | ||||||

|

Other Current Assets

|

$ | 20,175,435 | $ | 17,483,996 | $ | 418,482 | ||||||

|

Property and Equipment, Net

|

$ | 609,850 | $ | 290,665 | $ | 49,238 | ||||||

|

Other Assets

|

$ | 7,474,514 | $ | 5,959,400 | $ | 1,139,091 | ||||||

|

Intangibles

|

$ | 29,441,130 | $ | 7,328,331 | $ | - | ||||||

|

Goodwill

|

$ | 10,516,497 | $ | 5,707,580 | $ | - | ||||||

|

Total Assets

|

$ | 73,150,272 | $ | 38,873,927 | $ | 1,615,112 | ||||||

|

Total Current Liabilities

|

$ | 33,237,507 | $ | 27,440,258 | $ | 6,182,953 | ||||||

|

Total Long Term Liabilities

|

$ | 7,180,557 | $ | 5,136,801 | $ | - | ||||||

|

Common Stock

|

$ | 19,593 | $ | 28,189 | $ | 17,988 | ||||||

|

Additional Paid-In Capital

|

$ | 51,256,243 | $ | 21,517,362 | $ | 6,130,440 | ||||||

|

Due from Sysorex Consulting

|

$ | (665,554 | ) | $ | (665,554 | ) | $ | (665,554 | ) | |||

|

Accumulated other comprehensive income

|

$ | (5,525 | ) | $ | 3,048 | $ | - | |||||

|

Accumulated Deficit

|

$ | (16,294,161 | ) | $ | (13,105,962 | ) | $ | (8,842,558 | ) | |||

|

Stockholders’ Equity (Deficiency) Attributable to Sysorex Global Holdings Corp.

|

$ | 34,310,596 | $ | 7,777,083 | $ | (3,359,684 | ) | |||||

|

Non-Controlling Interest

|

$ | (1,578,388 | ) | $ | (1,480,215 | ) | $ | (1,208,157 | ) | |||

|

Total Stockholdings Equity (Deficiency)

|

$ | 32,732,208 | $ | 6,296,868 | $ | (4,567,841 | ) | |||||

|

Total Liabilities and Stockholders’ Equity

|

$ | 73,150,272 | $ | 38,873,927 | $ | 1,615,112 | ||||||

|

Proforma Stockholders' Equity (Deficiency) as of

|

||||||||||||

|

June 30,

|

December 31,

|

|||||||||||

|

2014

|

2013

|

2012

|

||||||||||

|

Common Stock

|

$

|

19,593

|

$

|

14,095

|

$

|

8,994

|

||||||

|

Additional Paid-In Capital

|

$

|

51,256,243

|

$

|

21,531,457

|

$

|

6,139,434

|

||||||

|

Due from Sysorex Consulting

|

$

|

(665,554)

|

$

|

(665,554

|

)

|

$

|

(665,554

|

)

|

||||

|

Accumulated other comprehensive income

|

$

|

(5,525)

|

$

|

3,048

|

-

|

|||||||

|

Accumulated Deficit

|

$

|

(16,294,161)

|

$

|

(13,105,962

|

)

|

$

|

(8,842,558

|

)

|

||||

|

Stockholders’ Equity (Deficiency) Attributable to Sysorex Global Holdings Corp.

|

$

|

34,310,596

|

$

|

7,777,083

|

$

|

(3,359,684

|

)

|

|||||

|

Non-Controlling Interest

|

$

|

(1,578,388)

|

$

|

(1,480,215

|

)

|

$

|

(1,208,157

|

)

|

||||

|

Total Stockholders Equity (Deficiency)

|

$

|

32,732,208

|

$

|

6,296,868

|

$

|

(4,567,841

|

)

|

|||||

We are subject to the informational requirements of the Securities Exchange Act of 1934 and file annual, quarterly and current reports and other information with the Securities and Exchange Commission. You can read our filings, including the registration statement of which this prospectus is a part, over the internet at the Security and Exchange Commission’s website at www.sec.gov. You may also read and copy any document we file with the Securities and Exchange Commission at its public reference facility at 100 F Street, N.E., Washington, D.C., 20549, on official business days during the hours of 10 a.m. to 3 p.m. You may also obtain copies of the documents at prescribed rates by writing to the Public Reference Section of the Securities and Exchange Commission at 100 F Street, N.E., Washington, D.C., 20549. Please call the Securities and Exchange Commission at 1-800-SEC-0330 for further information on the operation of the public reference facility. If you do not have Internet access, requests for copies of such documents should be directed to Ms. Wendy Loundermon, the Company’s Chief Financial Officer, at Sysorex Global Holdings Corp., 3375 Scott Blvd., Suite 440, Santa Clara, CA 95054; Tel: 703-356-2900.

Statements contained in this prospectus concerning the provisions of any documents are summaries of those documents and are not necessarily complete. We refer you to the documents filed with the SEC for more information.

Investing in our common stock involves a high degree of risk. Prospective investors should carefully consider the risks described below, together with all of the other information included or referred to in this prospectus, before purchasing shares of our common stock. There are numerous and varied risks that may prevent us from achieving our goals. If any of these risks actually occurs, our business, financial condition or results of operations may be materially adversely affected. In such case, the trading price of our common stock could decline and investors in our common stock could lose all or part of their investment.

Risks Related to Consolidated Operations

Since we have recently acquired Lilien Systems, Shoom and AirPatrol, it is difficult for potential investors to evaluate our future consolidated business.

We completed the Lilien Acquisition on March 20, 2013, the Shoom Acquisition on September 6, 2013 and the AirPatrol Acquisition on April 16, 2014. Therefore, our limited combined operating history makes it difficult for potential investors to evaluate our business or prospective operations or the merits of an investment in our securities. We are subject to the risks inherent in the financing, expenditures, complications and delays characteristic of a newly combined business. These risks are described below under the risk factor titled “Any future acquisitions that we may make could disrupt our business, cause dilution to our stockholders and harm our business, financial condition or operating results.” In addition, while the former members of Lilien, and the shareholders of Shoom and AirPatorol have indemnified the Company from any undisclosed liabilities there may not be adequate resources to cover such indemnity. Furthermore, there are risks that the vendors, suppliers and customers of these acquired entities may not renew their relationships for which there is no indemnification. Accordingly, our business and success faces risks from uncertainties inherent to developing companies in a competitive environment. There can be no assurance that our efforts will be successful or that we will ultimately be able to attain profitability.

Our ability to successfully execute our business plan may require additional debt or equity financing, which may otherwise not be available on reasonable terms or at all.

As of June 30, 2014, we had $4.9 million of cash on hand. On March 20, 2013, we entered into a revolving credit line for up to $5,000,000 from Bridge Bank, N.A. which was increased to $6,000,000 with a $750,000 term loan on August 29, 2013. As of June 30, 2014, the Company owed $4,581,691 under its revolving credit line and $624,995 under the term loan which matures August 27, 2016. According to our business plan we may need additional debt or equity financing. Future financings through equity offerings by us will be dilutive to existing stockholders. Also, the terms of securities we may issue in future capital transactions may be more favorable to new investors than our current investors. Newly issued securities may include preferences, superior voting rights, the issuance of warrants or other derivative securities, and the issuance of incentive awards under employee equity incentive plans, which may have additional dilutive effects. We may also be required to recognize non-cash expenses in connection with certain securities we may issue in the future such as convertible notes and warrants, which would adversely impact our financial condition and results of operations. Our ability to obtain needed financing may be impaired by factors, including the condition of the economy and capital markets, both generally and specifically in our industry, and the fact that we are not profitable, which could impact the availability or cost of future financing. If the amount of capital we are able to raise from financing activities, together with our revenues from operations, is not sufficient to satisfy our capital needs, we may need to reduce our operations accordingly.

Failure to manage or protect growth may be detrimental to our business because our infrastructure may not be adequate for expansion.

The Lilien, Shoom and AirPatrol Acquisitions require a substantial expansion of the Company’s systems, workforce and facilities. We may fail to adequately manage our anticipated future growth. The substantial growth in our operations as a result of the Lilien, Shoom and AirPatrol Acquisitions is expected to place a significant strain on our administrative, financial and operational resources, and increase demands on our management and on our operational and administrative systems, controls and other resources. For instance Lilien’s growth strategy includes broadening its service and product offerings, implementing an aggressive marketing plan and employing leading technologies. There can be no assurance that our systems, procedures and controls will be adequate to support our operations as they expand. We cannot assure you that our existing personnel, systems, procedures or controls will be adequate to support our operations in the future or that we will be able to successfully implement appropriate measures consistent with our growth strategy. As part of this growth, we may have to implement new operational and financial systems, procedures and controls to expand, train and manage our employee base, and maintain close coordination among our staff. We cannot guarantee that we will be able to do so, or that if we are able to do so, we will be able to effectively integrate them into our existing staff and systems.

To the extent we acquire other businesses, we will also need to integrate and assimilate new operations, technologies and personnel. The integration of new personnel will continue to result in some disruption to ongoing operations. The ability to effectively manage growth in a rapidly evolving market requires effective planning and management processes. We will need to continue to improve operational, financial and managerial controls, reporting systems and procedures, and will need to continue to expand, train and manage our work force. There can be no assurance that the Company would be able to accomplish such an expansion on a timely basis. If the Company is unable to affect any required expansion and is unable to perform its contracts on a timely and satisfactory basis, its reputation and eligibility to secure additional contracts in the future could be damaged. The failure to perform could also result in a contract terminations and significant liability. Any such result would adversely affect the Company’s business and financial condition.

We will need to increase the size of our organization, and we may experience difficulties in managing growth, which would hurt our financial performance.

In addition to employees hired from Lilien, Shoom, AirPatrol and any other companies which we may acquire, we will need to expand our employee infrastructure for managerial, operational, financial and other resources at the parent company level. Future growth will impose significant added responsibilities on members of management, including the need to identify, recruit, maintain and integrate additional employees. Our future financial performance and our ability to commercialize our product candidates and to compete effectively will depend, in part, on our ability to manage any future growth effectively.

In order to manage our future growth, we will need to continue to improve our management, operational and financial controls and our reporting systems and procedures. All of these measures will require significant expenditures and will demand the attention of management. If we do not continue to enhance our management personnel and our operational and financial systems and controls in response to growth in our business, we could experience operating inefficiencies that could impair our competitive position and could increase our costs more than we had planned. If we are unable to manage growth effectively, our business, financial condition and operating results could be adversely affected.

Our business depends on experienced and skilled personnel, and if we are unable to attract and integrate skilled personnel, it will be more difficult for us to manage our business and complete contracts.

The success of our business depends on the skill of our personnel. Accordingly, it is critical that we maintain, and continue to build, a highly experienced management team and specialized workforce, including software programs and sales professionals. Competition for personnel, particularly those with expertise in government consulting and a security clearance, is high, and identifying candidates with the appropriate qualifications can be costly and difficult. We may not be able to hire the necessary personnel to implement our business strategy given our anticipated hiring needs, or we may need to provide higher compensation or more training to our personnel than we currently anticipate. In addition, our ability to recruit, hire and indirectly deploy former employees of the U.S. Government is subject to complex laws and regulations, which may serve as an impediment to our ability to attract such former employees.

Our business is labor intensive and our success depends on our ability to attract, retain, train and motivate highly skilled employees, including employees who may become part of our organization in connection with our acquisitions. The increase in demand for consulting, technology integration and managed services has further increased the need for employees with specialized skills or significant experience in these areas. Our ability to expand our operations will be highly dependent on our ability to attract a sufficient number of highly skilled employees and to retain our employees and the employees of companies that we have acquired. We may not be successful in attracting and retaining enough employees to achieve our desired expansion or staffing plans. Furthermore, the industry turnover rates for these types of employees are high and we may not be successful in retaining, training or motivating our employees. Any inability to attract, retain, train and motivate employees could impair our ability to adequately manage and complete existing projects and to accept new client engagements. Such inability may also force us to increase our hiring of independent contractors, which may increase our costs and reduce our profitability on client engagements. We must also devote substantial managerial and financial resources to monitoring and managing our workforce. Our future success will depend on our ability to manage the levels and related costs of our workforce.

In the event we are unable to attract, hire and retain the requisite personnel and subcontractors, we may experience delays in completing contracts in accordance with project schedules and budgets, which may have an adverse effect on our financial results, harm our reputation and cause us to curtail our pursuit of new contracts. Further, any increase in demand for personnel may result in higher costs, causing us to exceed the budget on a contract, which in turn may have an adverse effect on our business, financial condition and operating results and harm our relationships with our customers.

We have allocated a substantial portion of the net proceeds of our initial public offering to expand our business, in part, through future acquisitions, but we may not be able to identify or complete suitable acquisitions, which could harm our financial performance.

Acquisitions are a significant part of our growth strategy. On April 9, 2014 we raised net proceeds of $17.7 million in our initial public offering from the sale of 3,166,666 Shares. Out of the net proceeds of our initial public offering we utilized approximately $10.5 million for the AirPatrol Acquisition. We continually review, evaluate and consider potential investments and acquisitions. In such evaluations, we are required to make difficult judgments regarding the value of business opportunities and the risks and cost of potential liabilities. We plan to use acquisitions of companies or technologies to expand our project skill sets and capabilities, expand our geographic markets, add experienced management and increase our product and service offerings. Although we have identified several acquisition considerations, we may be unable to implement our growth strategy if we cannot reach agreement with acquisition targets on acceptable terms or arrange required financing for acquisitions on acceptable terms. If we cannot make acquisitions to expand our business, our future financial performance could be harmed. In addition, the time and effort involved in attempting to identify acquisition candidates and consummate acquisitions may divert members of our management from the operations of our company, which could also harm our business and results of operations.

Any future acquisitions that we may make could disrupt our business, cause dilution to our stockholders and harm our business, financial condition or operating results.

If we are successful in consummating acquisitions, those acquisitions could subject us to a number of risks, including, but not limited to:

|

·

|

the purchase price we pay and/or unanticipated costs could significantly deplete our cash reserves or result in dilution to our existing stockholders;

|

|

|

|

·

|

we may find that the acquired company or technologies do not improve our market position as planned;

|

|

·

|

we may have difficulty integrating the operations and personnel of the acquired company, as the combined operations will place significant demands on the Company’s management, technical, financial and other resources;

|

|

|

|

·

|

key personnel and customers of the acquired company may terminate their relationships with the acquired company as a result of the acquisition;

|

|

|

·

|

we may experience additional financial and accounting challenges and complexities in areas such as tax planning and financial reporting;

|

|

|

·

|

we may assume or be held liable for risks and liabilities (including environmental-related costs) as a result of our acquisitions, some of which we may not be able to discover during our due diligence or adequately adjust for in our acquisition arrangements;

|

|

|

·

|

our ongoing business and management’s attention may be disrupted or diverted by transition or integration issues and the complexity of managing geographically or culturally diverse enterprises;

|

|

|

·

|

we may incur one-time write-offs or restructuring charges in connection with the acquisition;

|

|

|

·

|

we may acquire goodwill and other intangible assets that are subject to amortization or impairment tests, which could result in future charges to earnings; and

|

|

|

·

|

we may not be able to realize the cost savings or other financial benefits we anticipated.

|

We cannot assure you that we will successfully integrate Lilien, Shoom and AirPatrol or profitably manage any other acquired business. In addition, we cannot assure you that, following any acquisition, our continued business will achieve sales levels, profitability, efficiencies or synergies that justify the acquisition or that the acquisition will result in increased earnings for us in any future period. These factors could have a material adverse effect on our business, financial condition and operating results.

Insurance and contractual protections may not always cover lost revenue, increased expenses or liquidated damages payments, which could adversely affect our financial results.

Although we maintain insurance and intend to obtain warranties from suppliers, obligate subcontractors to meet certain performance levels and attempt, where feasible, to pass risks we cannot control to our customers, the proceeds of such insurance, warranties, performance guarantees or risk sharing arrangements may not be adequate to cover lost revenue, increased expenses or liquidated damages payments that may be required in the future.

If we are unable to comply with certain financial and operating restrictions in our credit facilities, we may be limited in our business activities and access to credit or may default under our credit facilities

Pursuant to our existing credit facility with Bridge Bank, N.A., all of the Company’s and our subsidiaries’ assets, other than excluded and future projects, are secured with our senior lender. As of June 30, 2014 the Company owed approximately $4.6 million under its revolving line of credit and $624,995 under a term loan. Provisions in our credit facilities and debt instruments impose restrictions or require prior approval on our ability, and the ability of certain of our subsidiaries to, among other things:

|

·

|

incur additional debt;

|

|

|

·

|

pay cash dividends and make distributions;

|

|

|

·

|

make certain investments and acquisitions;

|

|

|

·

|

guarantee the indebtedness of others or our subsidiaries;

|

|

|

·

|

redeem or repurchase capital stock;

|

|

·

|

create liens or encumbrances;

|

|

|

|

·

|

enter into transactions with affiliates;

|

|

|

·

|

engage in new lines of business;

|

|

|

·

|

sell, lease or transfer certain parts of our business or property;

|

|

|

·

|

incur obligations for capital expenditures;

|

|

|

·

|

issue additional capital stock of the Company or any subsidiary of the Company;

|

|

|

·

|

acquire new companies and merge or consolidate.

|

These agreements also contain other customary covenants, including covenants that require us to meet specified financial ratios and financial tests. We may not be able to comply with these covenants in the future. Our failure to comply with these covenants may result in the declaration of an event of default and cause us to be unable to borrow under our credit facilities and debt instruments. In addition to preventing additional borrowings under these agreements, an event of default, if not cured or waived, may result in the acceleration of the maturity of indebtedness outstanding under these agreements, which would require us to pay all amounts outstanding. If the maturity of our indebtedness is accelerated, we may not have sufficient funds available for repayment or we may not have the ability to borrow or obtain sufficient funds to replace the accelerated indebtedness on terms acceptable to us or at all. Our failure to repay our bank indebtedness would result in the bank foreclosing on all or a portion of our assets and force us to curtail our operations.

We may be subject to damages resulting from claims that the Company or our employees have wrongfully used or disclosed alleged trade secrets of their former employers.

Upon completion of any acquisitions by the Company, we may be subject to claims that our acquired companies and their employees may have inadvertently or otherwise used or disclosed trade secrets or other proprietary information of former employers or competitors. Litigation may be necessary to defend against these claims. Even if we are successful in defending against these claims, litigation could result in substantial costs and be a distraction to management. If we fail in defending such claims, in addition to paying money claims, we may lose valuable intellectual property rights or personnel. A loss of key research personnel or their work product could hamper or prevent our ability to commercialize certain products, which could severely harm our business.

The loss of our Chief Executive Offer or other key personnel may adversely affect our operations.

The Company’s success depends to a significant extent upon the operation, experience, and continued services of certain of its officers, including our CEO, as well as other key personnel. While our CEO and the executive officers of Lilien, Shoom and AirPatrol are all employed under employment contracts, there is no assurance we will be able to retain their services. The loss of our CEO or several of the other key personnel could have an adverse effect on the Company. If our CEO or other executive officers were to leave we would face substantial difficulty in hiring a qualified successor and could experience a loss in productivity while any successor obtains the necessary training and experience. Furthermore, we do not maintain “key person” life insurance on the lives of any executive officer and their death or incapacity would have a material adverse effect on us. The competition for qualified personnel is intense, and the loss of services of certain key personnel could adversely affect our business.

Internal system or service failures could disrupt our business and impair our ability to effectively provide our services and products to our customers, which could damage our reputation and adversely affect our revenues and profitability.

Any system or service disruptions, including those caused by ongoing projects to improve our information technology systems and the delivery of services, if not anticipated and appropriately mitigated, could have a material adverse effect on our business including, among other things, an adverse effect on our ability to bill our customers for work performed on our contracts, collect the amounts that have been billed and produce accurate financial statements in a timely manner. We are also subject to systems failures, including network, software or hardware failures, whether caused by us, third-party service providers, cyber security threats, natural disasters, power shortages, terrorist attacks or other events, which could cause loss of data and interruptions or delays in our business, cause us to incur remediation costs, subject us to claims and damage our reputation. In addition, the failure or disruption of our communications or utilities could cause us to interrupt or suspend our operations or otherwise adversely affect our business. Our property and business interruption insurance may be inadequate to compensate us for all losses that may occur as a result of any system or operational failure or disruption and, as a result, our future results could be adversely affected.

Customer systems failures could damage our reputation and adversely affect our revenues and profitability.

Many of the systems and networks that we develop, install and maintain for our customers involve managing and protecting personal information and information relating to national security and other sensitive government functions. While we have programs designed to comply with relevant privacy and security laws and restrictions, if a system or network that we develop, install or maintain were to fail or experience a security breach or service interruption, whether caused by us, third-party service providers, cyber security threats or other events, we may experience loss of revenue, remediation costs or face claims for damages or contract termination. Any such event could cause serious harm to our reputation and prevent us from having access to or being eligible for further work on such systems and networks. Our errors and omissions liability insurance may be inadequate to compensate us for all of the damages that we may incur and, as a result, our future results could be adversely affected.

Our financial performance could be adversely affected by decreases in spending on technology products and services by our public sector customers.

Our sales to our public sector customers are impacted by government spending policies, budget priorities and revenue levels. Although our sales to the federal government are diversified across multiple agencies and departments, they collectively accounted for approximately 10% of 2013 net sales. AirPatrol’s revenues are expected primarily from government customers in 2014 but are anticipated to shift toward a majority of commercial customers in the future. This could increase our consolidated 2014 revenues from government customers to increase to 15-20%. An adverse change in government spending policies (including budget cuts at the federal level), budget priorities or revenue levels could cause our public sector customers to reduce their purchases or to terminate or not renew their contracts with us, which could adversely affect our business, results of operations or cash flows.

Our business could be adversely affected by the loss of certain vendor partner relationships and the availability of their products.

We purchase products for resale from vendor partners, which include OEMs, software publishers, and wholesale distributors. For the year ended December 31, 2013, we purchased approximately 83% of the products we sold directly from vendor partners and the remaining amount from wholesale distributors. We are authorized by vendor partners to sell all or some of their products via direct marketing activities. Our authorization with each vendor partner is subject to specific terms and conditions regarding such things as sales channel restrictions, product return privileges, price protection policies and purchase discounts. In the event we were to lose one of our significant vendor partners, our business could be adversely affected.

We have entered, and expect to continue to enter, into joint venture, teaming and other arrangements, and these activities involve risks and uncertainties. A failure of any such relationship could have material adverse results on our business and results of operations.

We have entered, and expect to continue to enter, into joint venture, teaming and other arrangements. These activities involve risks and uncertainties, including the risk of the joint venture or applicable entity failing to satisfy its obligations, which may result in certain liabilities to us for guarantees and other commitments, the challenges in achieving strategic objectives and expected benefits of the business arrangement, the risk of conflicts arising between us and our partners and the difficulty of managing and resolving such conflicts, and the difficulty of managing or otherwise monitoring such business arrangements. A failure of our business relationships could have material adverse results on our business and results of operations.

Our business and operations expose us to numerous legal and regulatory requirements and any violation of these requirements could harm our business.

We are subject to numerous federal, state and foreign legal requirements on matters as diverse as data privacy and protection, employment and labor relations, immigration, taxation, anticorruption, import/export controls, trade restrictions, internal and disclosure control obligations, securities regulation and anti-competition. Compliance with diverse and changing legal requirements is costly, time-consuming and requires significant resources. We are also focused on expanding our business in certain identified growth areas, such as health information technology, energy and environment, which are highly regulated and may expose us to increased compliance risk. Violations of one or more of these diverse legal requirements in the conduct of our business could result in significant fines and other damages, criminal sanctions against us or our officers, prohibitions on doing business and damage to our reputation. Violations of these regulations or contractual obligations related to regulatory compliance in connection with the performance of customer contracts could also result in liability for significant monetary damages, fines and/or criminal prosecution, unfavorable publicity and other reputational damage, restrictions on our ability to compete for certain work and allegations by our customers that we have not performed our contractual obligations.

If we do not adequately protect our intellectual property rights, we may experience a loss of revenue and our operations may be materially harmed.

We have not registered copyrights on any of the software we have developed. We rely upon confidentiality agreements signed by our employees, consultants and third parties to protect our intellectual property. We cannot assure you that we can adequately protect our intellectual property or successfully prosecute actual or potential infringement of our intellectual property rights. Also, we cannot assure you that others will not assert rights in, or ownership of, trademarks and other proprietary rights of ours or that we will be able to successfully resolve these types of conflicts to our satisfaction. Our failure to protect our intellectual property rights may result in a loss of revenue and could materially adversely affect our operations and financial condition.

Our performance and ability to compete are dependent to a significant degree on our proprietary technology. Our proprietary software is protected by common law copyright laws, as opposed to registration under copyright statutes. Common law protection may be narrower than that which we could obtain under registered copyrights. As a result, we may experience difficulty in enforcing our copyrights against certain third party infringements. As part of our confidentiality-protection procedures, we generally enter into agreements with our employees and consultants and limit access to, and distribution of, our software, documentation and other proprietary information. There can be no assurance that the steps we have taken will prevent misappropriation of our technology or that agreements entered into for that purpose will be enforceable. The laws of other countries may afford us little or no protection of our intellectual property. We also rely on a variety of technology that we license from third parties. There can be no assurance that these third party technology licenses will continue to be available to us on commercially reasonable terms, if at all. The loss of or inability to maintain or obtain upgrades to any of these technology licenses could result in delays in completing software enhancements and new development until equivalent technology could be identified, licensed or developed and integrated. Any such delays would materially and adversely affect our business.

Risks Related to the Business and Industry of our Subsidiaries

Our growth is dependent on increasing sales to our existing clients and obtaining new clients, which, if unsuccessful, could limit our financial performance.

Our ability to increase revenues from existing clients by identifying additional opportunities to sell more of the products and services of our subsidiaries Lilien, Shoom and AirPatrol, and our ability to obtain new clients depends on a number of factors, including our ability to offer high quality products and services at competitive prices, the strength of our competitors and the capabilities of our sales and marketing departments. If we are not able to continue to increase sales to the existing clients of our subsidiaries or to obtain new clients in the future, we may not be able to increase our revenues and could suffer a decrease in revenues as well.

Our results depend on the continued growth of the market for IT products and services, which is uncertain.

Lilien’s IT products and services solutions are designed to address the growing markets for off-premises services (including migrations, consolidations, Cloud computing and disaster recovery), technology integration services (including storage and data protection services and the implementation of virtualization solutions) and managed services (including operational support and client support). These markets are still evolving. Competing technologies and services or reductions in corporate spending may reduce the demand for our products and services.

Decreases, or slow growth, in the newspaper publishing industry may adversely affect Shoom’s customers and negatively impact our results from the Shoom operations.

The newspaper industry as a whole is experiencing challenges to maintain and grow print circulation and revenues. This results from, among other factors, increased competition from other media, particularly the growth of electronic media, and shifting preferences among some consumers to receive all or a portion of their news other than from a newspaper. Shoom’s customer base is focused on the newspaper publishing industry and therefore its sales will be subject to the future of newspaper industry. Sysorex plans to help Shoom expand into other verticals but there is no guarantee that it will be successful and no way to know how long such an expansion will take.

Our competitiveness depends significantly on our ability to keep pace with the rapid changes in IT. Failure by us to anticipate and meet Lilien’s clients’ technological needs could adversely affect our competitiveness and growth prospects.

Lilien operates and competes in an industry characterized by rapid technological innovation, changing client needs, evolving industry standards and frequent introductions of new products, product enhancements, services and distribution methods. Our success depends on our ability to develop expertise with these new products, product enhancements, services and distribution methods and to implement IT solutions that anticipate and respond to rapid changes in technology, the IT industry, and client needs. The introduction of new products, product enhancements and distribution methods could decrease demand for current products or render them obsolete. Sales of products and services can be dependent on demand for specific product categories, and any change in demand for or supply of such products could have a material adverse effect on our net sales if we fail to adapt to such changes in a timely manner.

We operate in a highly competitive market and Lilien and Shoom may be required to reduce the prices for their products and services to remain competitive, which could adversely affect our results of operations.

Our industry is developing rapidly and related technology trends are constantly evolving. In this environment, we face significant price competition from our competitors. We may be unable to offset the effect of declining average sales prices through increased sales volumes and/or reductions in our costs. Furthermore, we may be forced to reduce the prices of the products and services we sell in response to offerings made by our competitors. Finally, we may not be able to maintain the level of bargaining power that we have enjoyed in the past when negotiating the prices of our services.

Lilien faces substantial competition from other national, multi-regional, regional and local value-added resellers and IT service providers, some of which may have greater financial and other resources than we do or that may have more fully developed business relationships with clients or prospective clients than we do. Many of our competitors compete principally on the basis of price and may have lower costs or accept lower selling prices than we do and, therefore, we may need to reduce our prices. In addition, manufacturers may choose to market their products directly to end-users, rather than through IT solutions providers such as us, and this could adversely affect our business, financial condition and results of operations.

Profitability of our subsidiaries Lilien, Shoom and AirPatrol is dependent on the rates we are able to charge for our products and services. The rates we are able to charge for our products and services are affected by a number of factors, including:

|

·

|

our clients’ perceptions of our ability to add value through our services;

|

|

|

·

|

introduction of new services or products by us or our competitors;

|

|

|

·

|

our competitors’ pricing policies;

|

|

|

·

|

our ability to charge higher prices where market demand or the value of our services justifies it;

|

|

|

·

|

procurement practices of our clients; and

|

|

|

·

|

general economic and political conditions.

|

If we are not able to maintain favorable pricing for our products and services, our results of operations could be adversely affected.

Lilien’s sales are subject to quarterly and seasonal variations that may cause significant fluctuations in our operating results, therefore period-to-period comparisons of our operating results may not be reliable predictors of future performance.

The timing of our revenues can be difficult to predict. Our sales efforts involve educating our clients about the use and benefit of the products we sell and our services and solutions, including their technical capabilities and potential cost savings to an organization. Clients typically undertake a significant evaluation process that has in the past resulted in a lengthy sales cycle, which typically lasts several months, and may last a year or longer. We spend substantial time, effort and money on our sales efforts without any assurance that our efforts will produce any sales during a given period.

In addition, many of our clients spend a substantial portion of their IT budgets in the second half of the year. Other factors that may cause our quarterly operating results to fluctuate include changes in general economic conditions and the impact of unforeseen events. We believe that our revenues will continue to be affected in the future by cyclical trends. As a result, you may not be able to rely on period-to-period comparisons of our operating results as an indication of our future performance.

A delay in the completion of our clients’ budget processes could delay purchases of the products and services of our subsidiaries, and have an adverse effect on our business, operating results and financial condition.

We rely on our clients to purchase products and services from us to maintain and increase our earnings, and client purchases are frequently subject to budget constraints, multiple approvals and unplanned administrative, processing and other delays. If sales expected from a specific client are not realized when anticipated or at all, our results could fall short of public expectations and our business, operating results and financial condition could be materially adversely affected.

Lilien’s profit margins depend, in part, on the volume of products and services sold. A failure to achieve increases in our profit margins in the future could have a material adverse effect on our financial condition and results of operations.

Given the significant levels of competition that characterize the IT reseller market, it is unlikely that Lilien will be able to increase gross profit margins through increases in its sales of IT products alone. Any increases in its gross profit margins in the future will depend, in part, on the growth of our higher margin businesses such as IT consulting and professional services. In addition, low margins increase the sensitivity of our results of operations to increases in costs of financing. Any failure by us to maintain or increase our gross profit margins could have a material adverse effect on our financial condition and results of operations.

Any failures or interruptions in our services or systems could damage our reputation and substantially harm our business and results of operations.

Our success depends in part on our ability to provide reliable remote services, technology integration and managed services to our clients. The operations of Lilien, which currently has its company data center located in Larkspur, California, and Shoom has its data center in Los Angeles, California, are susceptible to damage or interruption from human error, fire, flood, power loss, telecommunications failure, terrorist attacks and similar events. We could also experience failures or interruptions of our systems and services, or other problems in connection with our operations, as a result of:

|

·

|

damage to or failure of our computer software or hardware or our connections;

|

|

|

·

|